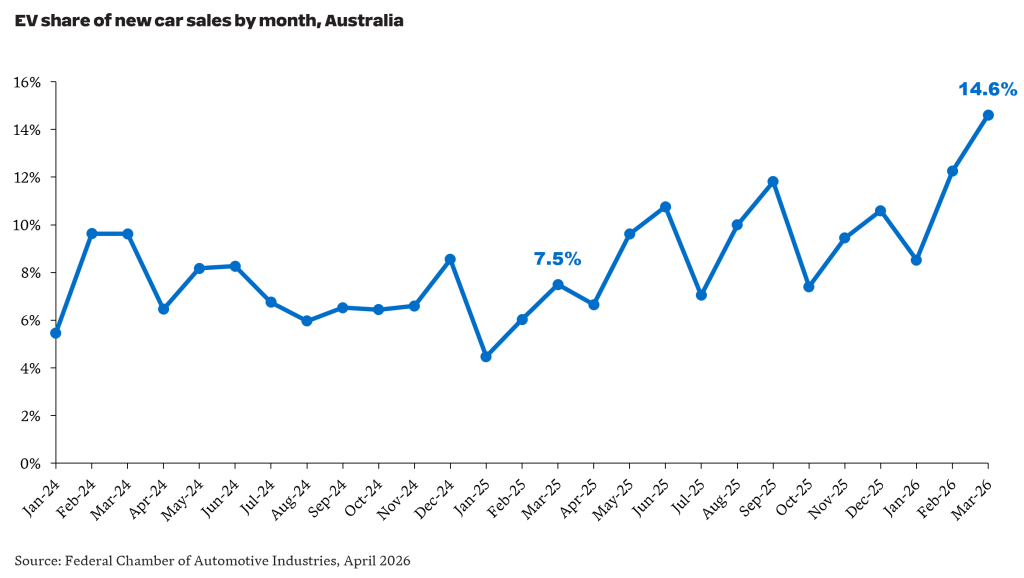

The current fuel crisis has materially accelerated Battery Electric Vehicle (EV) adoption in Australia. In March 2026, 16,000 new EVs were delivered, up from around 8,000 a year earlier. EV sales will continue to increase over the coming months. We explore what this means for motor insurers and provide some practical considerations.

The EV surge

EV sales as a proportion of all new car sales in Australia reached a new peak of 14.6% in March 2026, up from 7.5% in March 2025.

The acceleration in EV uptake is unsurprising. Analysis reported in The Australian showed the average cost per kilometre driven is over six times lower for EVs relative to Internal Combustion Engine (ICE) vehicles. For an EV, the cost was around $0.02. For an ICE vehicle, it was closer to $0.14 (excluding utes and large SUVs). The difference highlights the magnitude of the fuel/electricity cost difference. Of course, this doesn’t provide a complete picture of ownership cost differences. EVs are still on average more expensive than ICEs, but the gap is reducing and is expected to continue decreasing over time.

Implications for motor portfolios

While the EV share of motor portfolios is currently small (for example, EVs currently represent around 2% of IAG’s motor portfolio), a structural shift in the fleet composition, will have meaningful consequences for motor insurers.

A higher claim severity

EVs attract higher average repair costs than comparable ICE vehicles, due to a combination of:

- Repairs requiring specialist knowledge which attract higher labour rates and are often restricted to a limited network of authorised centres.

- Significant total loss exposure – EV battery packs continue to account for a high proportion of vehicle value (currently estimates in the 30%-50% range). Even minor collisions can trigger high repair costs where battery damage is found.

- EVs are typically equipped with Advanced Driver Assistance Systems (ADAS) and sensor suites, with high replacement and calibration costs.

A lower accident frequency, perhaps?

EVs sold tend to include more advanced safety technology than the average ICE vehicle on the road today and should in theory demonstrate a lower claim frequency. However, reports to date have been mixed. An analysis by Parmar and Woods (2025) of data from Norway reported a 17% lower accident frequency overall for EVs compared to ICE vehicles. This study focused on passenger vehicles and found EV frequency to be lower across most dimensions (e.g. type of accident, road type, speed limits, weather), but higher frequency in certain scenarios (e.g. pedestrian accidents and rear-end collisions).

How should insurers respond?

EV claims inflation is outpacing ICE vehicles due to battery costs and limited repair networks. As EV volumes grow, engaging with repairers early to ensure access to a sufficient network of certified repairers will be an important lever to managing claims cost.

How do EV and ICE premiums compare?

EVs typically cost more to insure than comparable ICE vehicles. Part of the reason is EVs tend to be more expensive than comparable ICE vehicles. However, this is only part of the story.

We’ve analysed quotes from NRMA, QBE and AAMI for three common ICE vehicles and three EVs with similar vehicle values. Our market scan showed each insurer offered a higher price for the EV relative to the comparable ICE variant – with the difference ranging from +0% to +39%. We also found a higher variation in premiums for EVs. For example, for the BYD Atto 3, we found a $900 difference between the cheapest and the most expensive premium. For the petrol Mazda CX-30, the difference was $500.

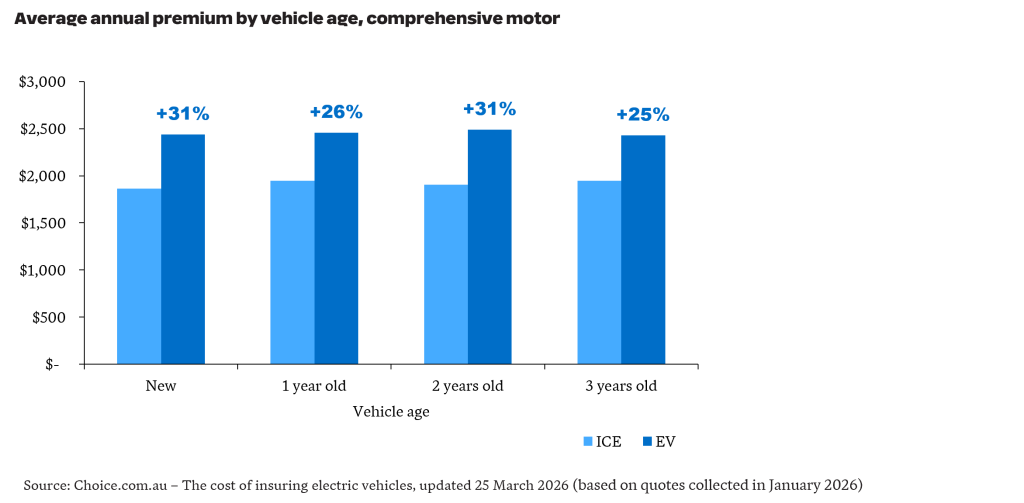

These results align with analysis by choice.com.au which compared the average annual comprehensive motor premium across 16,000 EVs and 36,000 ICE vehicles – showing EVs were up to 31% more expensive.

What insurers need to monitor to stay ahead

The fuel crisis may have done more than shift consumer behaviour in the short term – it may have pulled forward Australia’s EV transition by several years.

For motor insurers, the portfolio implications will compound over time and the developments warrant active monitoring. The major changes will be:

- Fleet composition drift – As EV penetration rises, the mix of vehicles on risk will continue to shift towards EVs. Insurers will need to consider the impact of changes in brand mix with several new manufacturers with little local claims history entering the market. Over the short to medium term, with the accumulation of local EV claims experience, insurers should be better placed to validate and revise assumptions currently embedded in their pricing – replacing assumptions informed by experience overseas or using non-EV proxies.

- Repairer costs and network expansion – The current higher EV repair costs is in part a product of repairer scarcity and parts supply immaturity. As the repair ecosystem develops, average EV claims costs should moderate – however the pace of this development is highly uncertain. Pricing models should be updated as experience emerges to maintain competitiveness and at the same time ensure pricing remains adequate.

- Government initiatives – EV uptake is materially impacted by government initiatives – in Germany, the US and China, material reductions in EV sales were observed following roll-back or removal of subsidies. For Australia, there is uncertainty around potential scaling back of the Fringe Benefits Tax exemption for EVs, at least until the May 2026 Budget. State government initiatives, such as the 2026 update to the NSW Electric Vehicle Strategy which includes extension of electrification incentives to commercial vehicles, training initiatives for EV mechanics and commitment of $100M to expand charging infrastructure, should accelerate EV adoption.

The fuel crisis may do more than temporarily alter driving behaviour. It could accelerate a lasting shift in Australia’s vehicle mix, bringing forward the transition to electric vehicles and reshaping motor portfolios sooner than many insurers expected. As EV exposure grows, insurers that respond early will be better placed to protect margins and retain market share.